This alert covers the new federal law limiting stretch IRA treatment following an owner’s death, required minimum distributions being suspended for 2020, and COVID-19-related distributions from IRAs.

Federal SECURE Act Now Requires Full Distribution of IRA Accounts Within 10 Years of Owner’s Death for Many Beneficiaries

Enacted into law at the end of 2019, the Setting Every Community Up for Retirement Enhancement (SECURE) Act imposes a number of changes to existing rules governing individual retirement accounts (IRAs).

These changes include, among others:

- Raising the age when required minimum distribution must begin to age 72, up from age 70 1/2

- Removing the age limit for IRA contributions

- Requiring the entire IRA to be distributed by the end of the 10th year following the year of the owner’s death for many beneficiaries

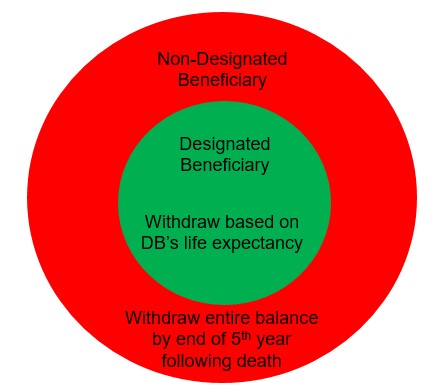

This shortened distribution requirement represents a significant departure from existing rules. Before the SECURE Act became law, any “designated beneficiary” had the ability to roll the IRA into an inherited IRA and take annual required minimum distributions (RMDs) over the designated beneficiary’s life expectancy. A designated beneficiary included any individual and certain types of trusts called “see-through” trusts. The life expectancy payout, an increasing percentage of the account’s value based on the beneficiary’s age, provides significant tax-deferral benefits for an individual or trust beneficiary.

A non-designated beneficiary—such as the owner’s estate or a charity—was generally required to withdraw the entire balance by the end of the fifth year after the owner’s death.

The following graphic illustrates the IRA withdrawal rules in the pre-SECURE Act environment:

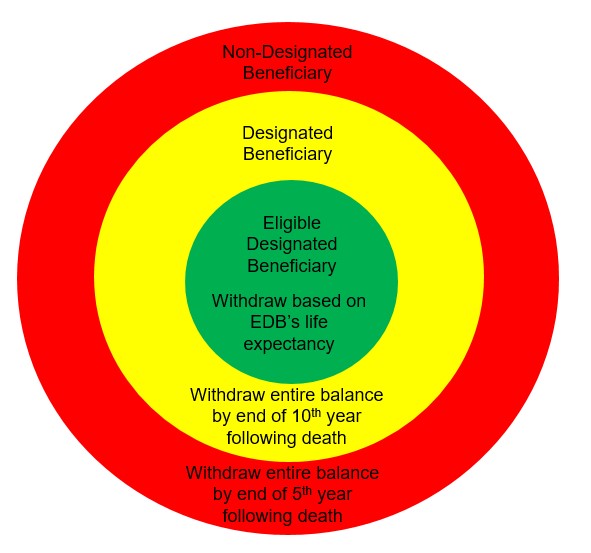

The SECURE Act created a new type of beneficiary called the “eligible designated beneficiary.” Under the SECURE Act, only eligible designated beneficiaries are able to take RMDs over their life expectancies.

Eligible designated beneficiaries include:

- The owner’s spouse

- The owner’s minor child (during the period of minority)

- Disabled individuals

- Chronically ill individuals

- A beneficiary who is not more than 10 years younger than the owner

For all other designated beneficiaries, the entire IRA must be withdrawn by the end of the 10th year following the year of the account owner’s death. The rules governing non-designated beneficiaries remain unchanged.

Note that for a minor child, upon reaching age 18 (or potentially until age 26, as long as the child is a full-time student) they no longer qualify as an eligible designated beneficiary. Once this status is lost, the life expectancy payout is no longer available, and the designated beneficiary rules requiring withdrawal by end of the 10th year following the year of majority will apply.

The following graphic illustrates the new withdrawal rules under the SECURE Act:

See-through trusts remain useful tools for both eligible designated beneficiaries and designated beneficiaries alike. Although IRA distribution timeframes will be accelerated in many circumstances, we continue to utilize trusts as beneficiaries of IRAs for various purposes, such as allowing for the protection of assets and control of the ultimate IRA distribution, with provisions designed to minimize income taxes as much as possible.

Given that the SECURE Act has minimized tax-deferral opportunities for many beneficiaries, it is more important than ever for an owner work with a skilled estate planning attorney to identify any tax-minimizing opportunities and to properly designate IRA beneficiaries in a way that effectuates the owner’s overall estate plan without adverse tax effects.

Required Minimum Distributions Suspended for 2020

As part of the the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the RMD rules for IRAs have been suspended for 2020. This means that instead of being required to withdraw and pay income tax on money from an IRA in 2020, retirees can keep their investments growing on an income-tax-deferred basis.

Beneficiaries with inherited IRAs who were previously required to withdraw an RMD are likewise permitted to waive their RMD for 2020.

Coronavirus-Related Distributions from IRAs

The CARES Act also allows for a penalty-free coronavirus-related distribution (CRD) of up to $100,000 in the aggregate from all of an owner’s IRAs or other “eligible retirement plans,” which includes pensions, 401(k)s, 403(b)s, and governmental 457(b) plans.

A CRD is a distribution made in calendar year 2020 to an individual who meets one of the following criteria:

- Who is diagnosed with COVID-19 or SARS-CoV-2

- Whose spouse or dependent is diagnosed with COVID-19 or SARS-CoV-2

- Who has experienced an adverse financial consequence as a result of being quarantined, furloughed, laid off, having work hours reduced due to COVID-19, or unable to work due to lack of child care or for business owners who are unable to work due to the closing or reduction of hours of their business

- Any other factors determined by the IRS or US Department of the Treasury

The CRD is taxed as ordinary income, and the participant may either elect to pay income taxes on the full amount in the year of distribution or spread the income ratably over a three-year period. Alternatively, the participant may repay the CRD within three years.

Barclay Damon’s trust and estate attorneys are well versed in the ever-changing rules governing retirement accounts, and we are here to assist you in crafting your overall estate plan and structuring your IRA beneficiary designations as part of that plan.

If you have any questions regarding the content of this alert, please contact Rachelle Nuhfer, counsel, at rnuhfer@barclaydamon.com; Matthew Eaves, associate, at meaves@barclaydamon.com; or another member of the firm’s Trusts & Estates Practice Area.